Your Ultimate Guide to Buying Motorcycle Insurance

One of the prerequisites of purchasing a motorcycle in Singapore is having motorcycle insurance. Yes, getting the insurance to cover third-party liability is mandatory, but the choice of what type of motorcycle insurance you get is completely up to you.

So how to decide which type of motorcycle insurance to get? This guide aims to help you understand the types of coverage available, what to consider to help you decide which is best for your biking needs, and how to keep your insurance premium low.

With this article, you’ll be able to shop for just the right motorcycle insurance that best fits your needs without “over-insuring”, and enjoy peace of mind knowing you’re getting exactly what you’re paying for.

3 Types of Motorcycle Insurance in Singapore

There are typically 3 types of motorcycle insurance offered by the various insurance providers in Singapore:

3 Reasons to Get Comprehensive Motorcycle Insurance

Full comprehensive motorcycle insurance is definitely the most expensive of the three. We’re talking about premiums that may be more than a thousand dollars, and you may be tempted to spend that money on bike modifications or aesthetically accessorising your motorbike instead. But here are 3 reasons why comprehensive motorcycle insurance is worth shelling out for:

1. Save on Repair Costs

Say, in order to avoid hitting another motorist, you crash your motorcycle into a tree. There’s no third-party liability in this scenario, but your bike is pretty banged up — and you’re dreading the bill the motorcycle workshop is going to send you once all the repairs are done. Comprehensive motorcycle insurance covers damages to your motorcycle in accidents, even if you were the ‘cause’ of the damage. This can save you from paying crazy repair costs out of pocket.

2. Stay Protected Against Non-Collision Damage

The odds of your motorcycle getting swept up in a hurricane in Singapore may be pretty low, but ending up with water damage after a flooding incident is not so uncommon in our country. Only comprehensive motorcycle insurance covers situations such as natural disasters or vandalism.

3. Start Anew with Help

Especially if you own a brand-new or high-end motorcycle, the cost of replacing or repairing such a valuable bike can be extremely high. Having comprehensive motorcycle insurance can ensure that you don’t suffer a major financial loss in these cases.

Consider Optional Add-Ons

Clearly, even though comprehensive motorcycle insurance is the most beneficial, the policy on its own doesn’t cover everything you may be concerned about. That’s why you should always consider the optional add-ons that an insurance provider may offer, on top of your base motorcycle insurance policy.

Optional add-ons offer additional protection tailored to your personal needs, riding habits, and specific risks that standard coverage may not address. These add-ons can enhance the scope of your policy, providing you with more customised protection. Here are some optional add-ons to consider, depending on how relevant they are to you:

- Pillion rider coverage (named)

- Additional rider coverage (named)

- Any rider coverage (unnamed)

- Roadside assistance

- Personal accident and/or medical expenses

- Total loss replacement

- NCD protection

7 Things to Consider When Choosing Motorcycle Insurance

1. What are your specific insurance coverage needs?

Not every rider will have the same needs. For example:

If you already have a fairly comprehensive personal accident health insurance, you may not need to get it as an add-on on top of your motorcycle insurance.

If you already have a membership with a towing service, or for Harley-Davidson riders, HOG Assist, then you probably don’t require additional roadside assistance either.

2. How deep are your pockets?

In the event of an accident, how much are you able to pay out of pocket to cover the repairs of your own motorcycle? If you’re hoping to get the support of your insurance company to help cover the repair costs, getting a comprehensive plan is definitely a good idea.

3. Read the fine print

Different insurance companies may offer what seems like similar coverage, but always read the insurance policy wordings and consider these questions:

- How much is the coverage in dollars for legal representation?

- What are the specific exclusions?

- Where are you covered under the geographical limitations?

- What are your personal responsibilities in the event of an accident?

- How much excess are you agreeing to?

- Does the insurance cover LTA-approved modifications?

- Can you take your motorcycle to any workshop or only to a specific list of workshops?

4. Ask all your questions

If possible, approach an insurance agent to explain and break down what is included — and isn’t included — in the motorcycle insurance policy you’re considering. Make sure to ask ALL your questions — no questions are dumb questions when you’re deciding to sign up with motorcycle insurance. After all, most insurance companies actually reward your loyalty when you renew year after year, so it’s important to make the smart decision right from the jump.

5. Find out which USP appeals to you the most

Each insurance company tends to offer something different just to stand out from the crowd. However, this unique selling point (USP) differs from company to company. Find out what each company offers, then consider which offer meets your personal riding needs the most.

For example, most people automatically assume that the highest No Claim Discount (NCD) they can get is 20%. But DirectAsia actually offers NCD of up to 30%, the highest NCD cover in Singapore. If this is something that appeals to you, then find out more by getting a personal motorcycle insurance quote.

6. “Got promo or not?”

It’s natural for us Singaporeans to go where the better deal is. Some insurance companies may offer enticing promotions only for a limited duration to persuade you to sign up with their plans. If it’s a promotion that you could really benefit from, what’s the harm in examining them closely and picking the best promotion and policy that fits your needs?

For example, you can enjoy free Shell vouchers or free vehicle inspection at Vicom when you sign up with DirectAsia insurance.

7. Price is not the most important factor

Yes, even more than special promotions, we love savings. But remember that the lowest price may not always be the best deal or value-for-money. Thinking about the insurance process itself is also important — so if the insurance provider is known for great customer service, dedicated claims specialists, or an easy claims procedure, it may be worth the money you’re paying.

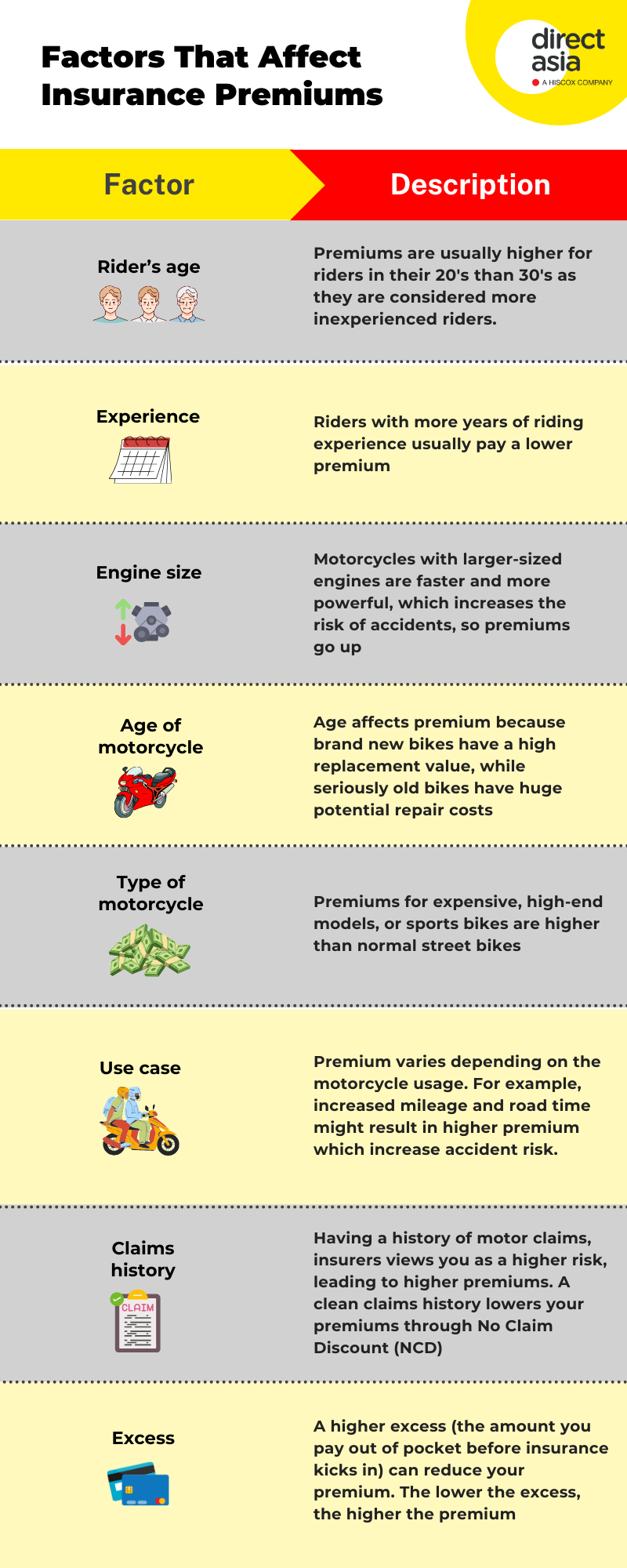

Understand the Factors that Affect Your Insurance Premium

Even if two motorcycle riders get a similar type of motorcycle insurance from the same insurance provider, they may end up paying different premium amounts. Why? First, you have to understand the factors that affect insurance premiums.

3 Tips to Keep your Insurance Premium Low

Understanding the factors that affect how much you’ll need to pay for your insurance premium also gives you clues as to how to keep your premium low. Here are 3 tips to consider:

1. Take Advantage of NCD

If you are not a new rider and have ridden safely for a few consecutive years and have not been in any accidents or made any insurance claims, you might be eligible for NCD.

But here’s where it gets interesting: Even if you’re buying your own motorcycle for the very first time, you can still claim NCD if you were riding a company motorcycle before, or if you previously lived overseas and rode a motorcycle there as well. All you would need to transfer your NCD is a letter from your HR department or previous motorcycle insurance company.

2. Stick to the Basics

If you’re looking to get a motorcycle for daily commutes, consider getting a standard street motorcycle over a flashy sports motorbike. Don’t go for large engine sizes if that’s not really what you need. This will save you money overall — not just in insurance premiums but also purchase price, COE, and road tax.

3. Review Your Insurance Annually

Things change, and so do your insurance needs. Regularly reviewing your policy — a good time is when it’s almost renewal time — helps ensure that you’re not paying for coverage you no longer need. For example, if your motorbike is no longer used by another rider, update your policy to reflect this and lower your premium.

DirectAsia Motorcycle Insurance

Why choose DirectAsia for your motorcycle insurance?

✅ All 3 types of motorcycle insurance at affordable rates

✅ Variety of optional add-ons to suit your biking needs

✅ More than 90% customer satisfaction rate

✅ Feefo Official Platinum Trusted Service Award 5 years in a row

✅ Highest NCD on the market at 30%

✅ List of partner motorcycle workshops islandwide that guarantee quality repairs